Pakistan is set to launch $500 million (£384m) in Islamic bonds to raise money for its foreign exchange reserves, a senior official said on Wednesday (September 28), as a three-year IMF bailout package nears a close.

The government has started looking at key markets for the ‘Sukuk’ bonds – a sharia-compliant instrument that offers profits instead of interest to its subscribers, a top official said.

“We have begun the roadshow in Dubai today and will go to London, Boston, and New York in the same leg,” Pakistan’s finance secretary Waqar Masood Khan told reporters.

The announcement comes as a three-year, $6.6-billion-dollar (£5bn) bailout package from the International Monetary Fund (IMF) comes to an end.

The lender announced in August it would soon release the last instalment, worth $102m (£78m).

Khan said the country needs to tap the global capital market to maintain its foreign exchange reserves, which currently stand at $22.69bn (£17.43bn), enough to cover import bills for five months.

“The purpose of the issuance of Sukuk bonds is to meet our growing future demand of the forex,” he said.

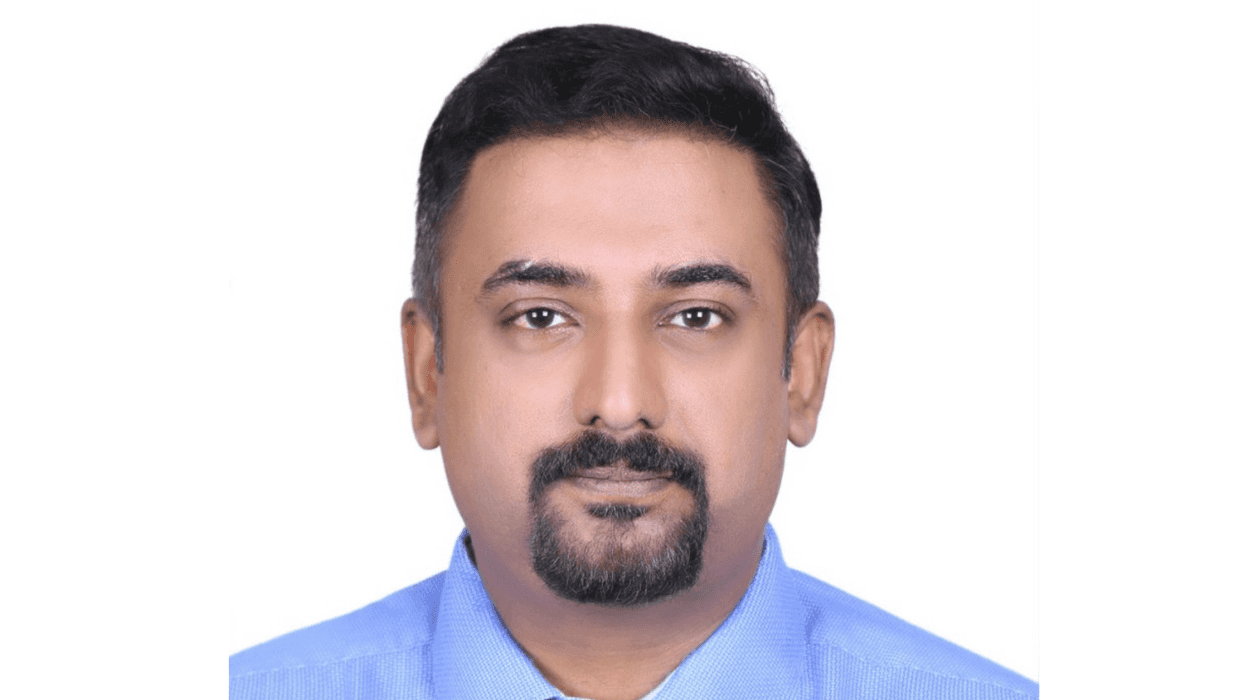

“After the IMF package is over and amid falling exports, Pakistan needs to raise the funds from different sources,” Rehan Ateeq, head of research at Shajar Capital added.

The move also comes as $1bn worth of 10-year Eurobonds draws to a close.

“We expect with the maturity of the IMF loan as well as the Eurobond, the government would come up with more such bonds soon,” Ateeq said.

Pakistan has so far issued Eurobonds and Sukuk worth $4.05bn (£3.11bn). It expects its economy to grow at 5.5 per cent in the the current fiscal year, compared to 4.7 per cent growth in the previous 12 months.